Last Updated: April 2026 (Updated to reflect current Canadian auto refinancing trends and lender requirements.)

Published: January 2025

By: Danielle Burton

Category: Credit, Co-Signers

When you apply for an auto loan with a co-signer in Canada, lenders don’t rely on just one credit score. Instead, they assess both applicants together to understand overall credit risk and loan eligibility.

But it’s not as simple as choosing the higher score.

Auto lenders review your credit, income, debts, and payment history to decide approval, interest rates, and loan terms. This is especially important for borrowers exploring auto financing options or applying for a bad credit auto loan with a co-signer in Canada.

Quick Answer: For a car loan with a co-signer, lenders review both credit scores but often place more weight on the stronger profile when making approval and pricing decisions. That said, both applicants share full payment responsibility, and both credit profiles influence the final outcome.

In This Guide:

- 1. Key Insights Before You Apply

- 2. Whose Credit Score Is Used When Buying a Car With a Co-Signer

- 3. What Happens When You Apply for a Car Loan With a Co-Signer in Canada

- 4. How Do Lenders Weigh Income, Debt, and Credit Between Two Applicants?

- 5. When Does a Co-Signer Actually Improve Your Approval Chances?

- 6. Can a Co-Signer Lower Your Interest Rate, or Just Help You Get Approved?

- 7. Who Builds Credit on a Co-Signed Car Loan, and Who Takes the Risk?

- 8. What Happens If Payments Are Missed on a Co-Signed Car Loan?

- 9. Can You Remove a Co-Signer From a Car Loan Later?

- 10. When Is Using a Co-Signer a Smart Move, and When Should You Avoid It?

- 11. Final Thoughts: Should You Use a Co-Signer or Explore Other Options?

- 12. Common Questions About Co-Signed Car Loans in Canada

1. Key Insights Before You Apply

Before applying for an auto loan with a co-signer in Canada, it’s important to understand how lenders assess approval, risk, and affordability.

Here’s what matters most:

- A co-signer can improve approval chances, especially for a first-time borrower or someone with limited credit history

- Lenders assess both the primary applicant and co-signer using information from credit bureaus, income, and existing financial obligations

- Stronger profiles can help reduce credit risk and may lead to better interest rates, but results vary by lender

- Monthly payments must fit within your budget after all current loan and credit commitments are considered

- The loan agreement is shared, meaning both applicants take on full payment responsibility from the start

In many cases, co-signed applications are used to support auto financing approvals when applying through banks, auto lenders, or auto dealers.

Understanding these factors can help you make a more informed decision before choosing to cosign a loan.

2. Whose Credit Score Is Used When Buying a Car With a Co-Signer

Do lenders use both credit scores or focus on one?

When buying a car with a co-signer, lenders review both credit scores, but they don’t treat them equally in every situation. Instead of averaging scores, auto lenders assess how each profile contributes to overall credit risk and often place more weight on the stronger applicant.

How Credit Is Actually Evaluated

Lenders review each person’s credit first, then evaluate the application as a whole. They typically look at:

- Credit reports from major credit bureaus

- Payment habits and consistency over time

- Length of credit history

- Any negative items, such as missed payments or accounts sent to a collection agency

A higher credit score can strengthen the application, but it doesn’t eliminate risk from the other borrower.

What This Means: A co-signed auto loan is not based on one credit score, it’s based on how both profiles work together.

- The stronger profile can improve approval and pricing

- The weaker profile can still influence loan terms

- The final decision reflects the combined level of risk

This is why understanding both credit profiles is important before applying.

3. What Happens When You Apply for a Car Loan With a Co-Signer in Canada

When you apply for a joint auto loan, lenders evaluate both the primary applicant and co-signer together as one financial profile. The goal is to reduce risk and ensure the loan is affordable.

What Lenders Review

- Credit history and payment behaviour

- Income and employment stability

- Existing financial obligations and monthly payments

Lenders may check paperwork, bank statements, and credit reports to verify details, confirm income, and assess your ability to repay.

After Approval

If approved, both applicants are equally tied to the loan agreement.

- The loan appears on both credit profiles

- Payment responsibility is shared

- Payment activity affects both applicants

From a lender’s perspective, both parties are fully accountable from the start.

4. How Do Lenders Weigh Income, Debt, and Credit Between Two Applicants?

For a co-signed auto loan in Canada, lenders look beyond credit scores and focus heavily on affordability.

Income, debt levels, and overall financial stability often play a bigger role in loan eligibility than credit score alone.

The Core Factors Lenders Review

When evaluating a joint application, auto lenders assess how both applicants support the loan together.

Key factors include:

- Income → Is there enough combined income to support the loan?

- Debt levels → What financial obligations does each applicant already carry?

- Debt-to-income ratio (DTI) → How much of monthly income is committed to existing payments?

- Employment stability → Is income consistent and reliable over time?

These factors help determine whether monthly payments will be manageable under the loan agreement.

How Income Is Assessed

In many cases, lenders combine income from both applicants, but not all income is weighted equally.

- Stable, verifiable income carries more value

- One strong income can support approval if the other is limited

- Higher income may be offset by higher debt

To confirm this, lenders may review bank statements and supporting loan paperwork to verify income and assess repayment capacity.

Why Debt Plays a Critical Role

Even with a strong co-signer, high debt levels can limit approval or affect loan terms.

- Existing loans increase overall credit risk

- High monthly payments reduce affordability

- Lenders prioritize balance over total income

This is why some co-signed auto financing applications are approved with higher interest rates or adjusted terms.

How Lenders Assess the Full Picture

Lenders don’t evaluate income, debt, and credit separately, they look at how everything works together.

- Strong income + low debt = higher approval potential

- High income + high debt = increased risk

- Balanced profiles = stronger application overall

Final approval and loan structure depend on whether the combined financial profile supports long-term repayment.

5. When Does a Co-Signer Actually Improve Your Approval Chances?

A co-signer can improve your chances of approval, but only when they meaningfully strengthen your loan eligibility. For an auto loan, lenders are looking for reduced credit risk, not just an additional name on the application.

When a Co-Signer Makes the Biggest Impact

A co-signer is most effective when they help fill a clear gap in the primary applicant’s profile.

This often includes:

- Limited or no credit history, especially for a first-time borrower

- Lower credit score with otherwise stable income

- Insufficient income to support monthly payments

- Short or inconsistent employment history

In these cases, the co-signer helps balance the application and improves how auto lenders view repayment ability.

When a Co-Signer May Not Improve Approval

There are situations where adding a co-signer has little impact on the outcome.

- Both applicants have high financial obligations

- Income is unstable or difficult to verify

- The loan amount is too high for the combined profile

- Negative credit activity exists across both applicants

If overall risk remains high, a co-signer may not significantly improve approval or loan terms.

What Auto Lenders Are Looking For

Lenders are not just adding a second applicant, they are evaluating whether the application becomes stronger overall.

They focus on:

- Improved affordability based on combined income

- More consistent payment habits

- A balanced financial profile with manageable risk

If these areas improve, approval becomes more likely.

A Practical Way to Think About It

A co-signer should strengthen the structure of the auto financing application.

- They should fill a gap, not duplicate weaknesses

- Their profile should improve stability and reduce risk

- The combined application should clearly support the loan agreement

If those conditions are met, a co-signer can meaningfully improve approval outcomes when working with auto lenders or auto dealers.

6. Can a Co-Signer Lower Your Interest Rate, or Just Help You Get Approved?

A co-signer can help you get approved for an auto loan and may also help lower your interest rate , depending on how much they reduce overall credit risk.

Auto lenders base interest rates on risk. The lower the risk, the better the potential rate. A strong co-signer may help by:

- Strengthening the overall credit profile

- Supporting affordability through income

- Demonstrating consistent payment habits

If the application still carries some risk, a co-signer may help you get approved but not lower the rate much.

This is why comparing offers from multiple auto lenders or auto dealers is important when exploring auto financing options.

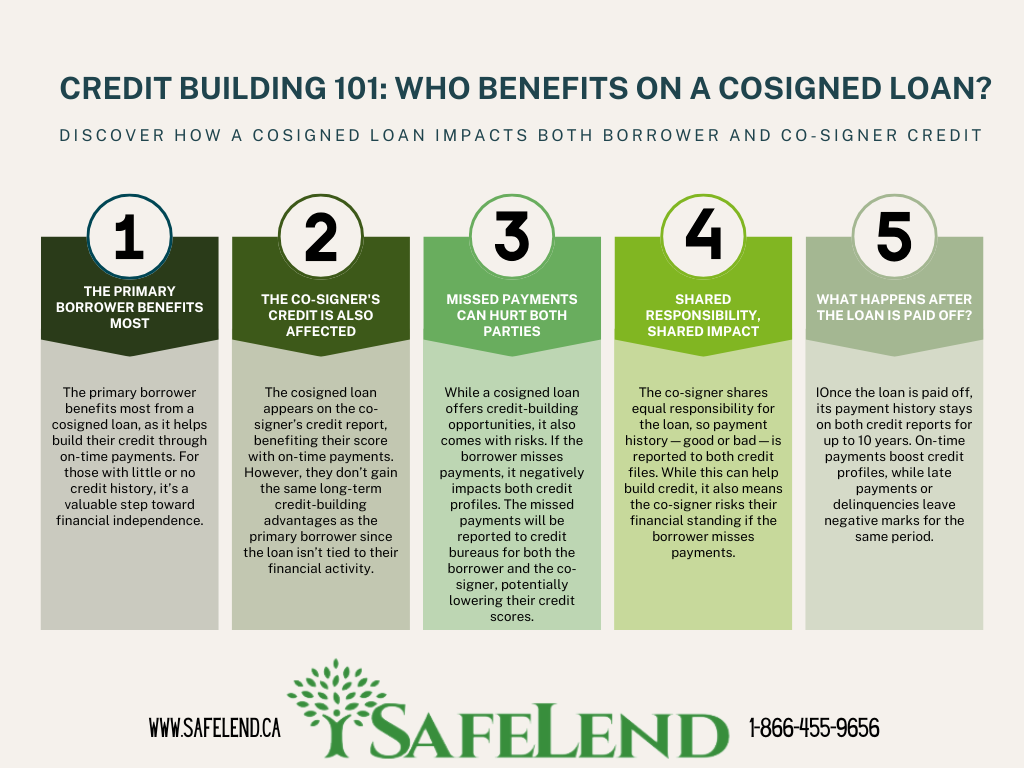

7. Who Builds Credit on a Co-Signed Car Loan, and Who Takes the Risk?

For a co-signed auto loan in Canada, both the primary applicant and co-signer build credit and share full payment responsibility under the loan agreement.

From the start, lenders treat the loan as a shared commitment, meaning both profiles are impacted equally over time.

How Credit Building Works

Once the loan is active, it is reported to major credit bureaus for both applicants.

- On-time payments can help improve both credit scores

- Consistent payment habits strengthen long-term credit profiles

- Positive performance benefits both the main borrower and co-signer

In many cases, a co-signed auto loan can help a first-time borrower establish credit when managed responsibly.

How Risk Is Shared

Along with the benefits, both applicants take on equal financial risk.

- Missed payments affect both credit reports

- The full loan balance appears on both profiles

- Lenders can pursue either borrower for repayment if needed

Even if payments are made through one account, such as a joint account or individual setup, responsibility does not change.

What This Means for Your Credit Profile

Whether payments are made by one person or shared, both applicants are affected by the outcome.

- Strong payment habits can improve both profiles

- Negative activity can lower both credit scores

- The loan contributes to overall debt and future borrowing capacity

Because of this, a co-signed auto loan should always be treated as a shared financial obligation from the beginning.

8. What Happens If Payments Are Missed on a Co-Signed Car Loan?

Missing payments affects both the main borrower and co-signer immediately, regardless of who was responsible for making the payment.

From a lender’s perspective, payment responsibility is shared under the loan agreement, so any missed or late payment is reported to both credit profiles.

Immediate Impact

When a payment is missed, auto lenders may:

- Report the late payment to credit bureaus

- Apply late fees or penalties

- Increase the perceived credit risk of the account

Even one missed payment can hurt your chances of getting approved in the future, especially if payments aren’t consistent. In more serious situations, payment default can lead to repossession, where the lender enforces the security of the lien tied to the vehicle.

Longer-Term Credit Impact

If missed payments continue, the consequences become more significant.

- Credit scores can drop due to repeated late payments

- Accounts may be transferred to a collection agency

- Negative history can remain on credit reports for years

This can impact both applicants’ ability to qualify for future auto financing or other credit products.

What Happens if the Loan Defaults

If payments stop completely, the lender may take further action.

- Either borrower can be pursued for the full remaining balance

- The vehicle may be repossessed and sold

- Any remaining balance after sale may still be owed

At this stage, both financial and credit recovery becomes more challenging.

How to Reduce the Risk

To avoid these outcomes, it’s important to manage the loan proactively.

- Set clear expectations before you cosign a loan

- Monitor payments regularly, even if one person is handling them

- Address financial issues early before they lead to missed payments

Taking a proactive approach can help protect both borrowers and maintain stronger credit profiles over time.

9. Can You Remove a Co-Signer From a Car Loan Later?

Yes, a co-signer can be removed from an auto loan, but it does not happen automatically. The primary borrower must qualify for a new loan on their own before the co-signer can be released from the loan agreement.

Until that happens, both parties remain fully responsible.

The Most Common Way to Remove a Co-Signer

The most common approach is through auto refinance.

- The primary applicant applies for a new auto loan independently

- A new lender pays off the existing loan

- The co-signer is removed once the new agreement is finalized

This process replaces the original loan with new loan paperwork under a single borrower.

When Removal Is More Likely

Lenders will only approve this change if the borrower can now support the loan on their own.

This typically includes:

- Improved credit profile since the original approval

- Stable income and manageable financial obligations

- Lower overall debt levels

- Consistent payment habits over time

The goal is to demonstrate reduced credit risk without the need for a co-signer.

When It May Not Be Possible Yet

In some situations, removing a co-signer may not be approved right away.

- Income may still be insufficient to support monthly payments

- Credit may not have improved enough

- Debt levels may still be too high

- The loan balance may still be large relative to income

In these cases, additional time and financial progress are usually needed before reapplying.

What to Keep in Mind

Removing a co-signer is not a simple request, it’s a new loan eligibility decision.

- Approval depends on your current financial position

- Timing plays an important role in success

- Preparation can improve your chances of approval

Planning ahead can help you transition from a co-signed loan to independent auto financing more smoothly.

10. When Is Using a Co-Signer a Smart Move, and When Should You Avoid It?

Using a co-signer for an auto loan can be a helpful strategy, but it works best when it clearly improves your loan eligibility and overall financial position.

The key is knowing when it adds value and when it may introduce unnecessary risk.

When Using a Co-Signer Makes Sense

A co-signer can be a strong option when it helps move your auto financing application forward.

- You’re struggling to qualify for an auto loan on your own

- You’re a first-time borrower or have limited credit history

- Your income alone does not support the required monthly payments

- You’re working to rebuild credit and improve your financial profile

In these situations, a co-signer can help reduce credit risk and create access to more manageable loan terms.

When You May Want to Avoid It

There are times when adding a co-signer may not be the best approach.

- You already meet loan eligibility requirements independently

- The co-signer does not significantly improve your application

- Financial obligations or risk could impact your relationship

- Your situation is likely to change in the near future

If the benefit is minimal, it may be worth exploring other auto financing options first.

Questions to Ask Before Moving Forward

Before choosing to cosign a loan, take a step back and assess the full picture.

- Will this improve both approval and long-term affordability?

- Can I realistically maintain consistent payment habits?

- Do I have a plan to refinance or remove the co-signer later?

- Is everyone comfortable with shared payment responsibility?

These questions help ensure the decision supports your long-term financial goals.

A Strategic Approach

A co-signer should be part of a plan, not just a quick solution.

- It can help you access better options through auto lenders or auto dealers

- It should support long-term financial improvement

- It works best when paired with a plan for future independence

Taking a thoughtful approach can help you benefit from a co-signed auto loan while minimizing risk.

11. Final Thoughts: Should You Use a Co-Signer or Explore Other Options?

A co-signer can open the door to auto financing when approval feels out of reach, but it works best when it supports a clear, long-term plan.

Key Takeaways

- Both applicants are evaluated together as part of one auto loan application

- A stronger profile can improve approval and influence loan terms

- Monthly payments must align with your budget and existing obligations

- Payment responsibility is shared under the loan agreement

- Removing a co-signer later typically requires auto refinance

Working with platforms like SafeLend Canada allows you to explore options with a soft credit check, compare offers from multiple auto lenders, and find a loan structure that fits your budget and goals.

12. Common Questions About Co-Signed Car Loans in Canada

Can a co-signer help you get approved with bad credit?

Yes, a co-signer can improve auto loan approval chances, especially if they have a stronger credit profile and stable income. Auto lenders may be more willing to approve the loan when overall credit risk is reduced, even if the primary applicant has lower credit.

Will a co-signed auto loan show up on both credit reports?

Yes, a co-signed auto loan is reported to credit bureaus for both applicants. Payment activity, including on-time or missed payments, will impact both credit profiles.

Does a co-signer have ownership of the vehicle?

Not necessarily. A co-signer is responsible for the loan and payments, but ownership depends on how the vehicle is registered. In some cases, only the main borrower is listed as the owner.

Can a co-signer be added after an auto loan is approved?

In most cases, no. To add a co-signer, a new application or auto refinance is required, along with updated loan paperwork under a new agreement.

Is a co-signer the same as a guarantor?

No. When you cosign a loan, both parties share full payment responsibility from the start. A guarantor may only become responsible if there is payment default, depending on the terms of the agreement.

How long does a co-signer stay on an auto loan?

A co-signer remains on the loan for the full term unless the loan is paid off or replaced through auto refinance. There is no automatic removal.

Can a co-signed loan affect future borrowing?

Yes, a co-signed auto loan is included in both applicants’ financial obligations. This can impact future loan eligibility, especially if monthly payments are high or if there is negative payment history.

What credit score is typically needed for a co-signer?

There is no fixed requirement, but auto lenders look for a co-signer with a stronger and more stable credit profile than the primary borrower. Higher and more consistent credit helps reduce overall credit risk.

Can you refinance a co-signed auto loan to remove the co-signer?

Yes, auto refinance is the most common way to remove a co-signer. The primary applicant must qualify independently for the new loan before the co-signer is released.

Is it better to apply with or without a co-signer?

It depends on your financial situation. If you meet loan eligibility requirements on your own, a co-signer may not be necessary. If not, a co-signer can help improve approval chances and access better auto financing options.

Does a down payment help when applying with a co-signer?

Yes, a down payment can reduce the loan amount, lower monthly payments, and improve approval chances by reducing overall risk for lenders.

Important Note: This article and its resources are purely for informational use. They do not reflect the offerings of specific companies or lenders. Our goal is to provide knowledge and insights for better financial decision-making. We recommend conducting in-depth research and seeking professional advice before making any financial decisions. SafeLend Canada, while not a lender, collaborates with various lenders to assist clients in refinancing their auto loans.