Last Updated: May 2026 (Updated to reflect current Canadian auto refinancing trends and lender requirements.)

Published: March 2025

By: Danielle Burton

Category: Vehicle Ownership

Buying your first car is a major milestone, but making the right decision goes beyond choosing the vehicle you want to drive. Every step in the car-buying process, from understanding the purchase price and monthly payments to reviewing your credit profile and credit score, plays a role in your long-term financial success.

Vehicle ownership means taking full financial and legal responsibility for a car, including payments, auto insurance, maintenance, and long-term value.

Understanding these responsibilities early helps you make smarter decisions and identify opportunities for a lower cost of ownership over time, whether you're comparing used cars or exploring the latest new cars in today’s evolving Canadian market.

Whether you're considering auto financing, leasing, or buying a vehicle outright, understanding your available financing options, including working with traditional lenders or online lenders, can help you avoid costly mistakes. Expenses like auto insurance, maintenance, and unexpected repairs can quickly add up, making it essential to understand the full cost of ownership before committing.

This guide walks first-time buyers through the entire process, from comparing buying options and reviewing contracts to completing ownership transfer, vehicle registration, and required documentation. You’ll also learn how different purchase paths, including private sellers and dealerships, can impact your experience and overall cost.

We’ll break down how factors like market conditions and your credit profile influence financing terms, and how tools like a vehicle history report or resources such as Kelley Blue Book can help you evaluate pricing and avoid overpaying in today’s competitive Canadian car-buying market.

By the end, you’ll have a clear understanding of how to navigate buying your first car in Canada, manage the total cost of owning a car, and move forward with confidence, while also learning how responsible financing can help you build your credit over time.

In This Guide:

- 1. What Does Vehicle Ownership Really Mean?

- 2. How Much Does Vehicle Ownership Really Cost in Canada?

- 3. What Is Vehicle Depreciation and Why Does It Matter?

- 4. How Do You Choose the Right Car for Your Budget and Needs?

- 5. Should You Finance, Lease, or Buy a Car Outright?

- 6. How Do Car Loans Work in Canada?

- 7. What Mistakes Should First-Time Car Buyers Avoid?

- 8. What Are the Hidden Costs of Vehicle Ownership (And How Can You Prepare)?

- 9. What Are the Steps to Buying a Car in Canada?

- 10. Final Thoughts: How Can You Make a Smart Car Buying Decision?

- 11. Frequently Asked Questions

What Does Vehicle Ownership Really Mean?

Vehicle ownership goes beyond simply having your name on a car. It represents full responsibility for how that vehicle is financed, maintained, and managed over time. Whether you’re purchasing through dealer financing, arranging your own auto financing, or paying upfront, the decisions you make early will shape your long-term financial outcome.

For first-time buyers, ownership involves more than just monthly payments. It includes ongoing expenses like car insurance, fuel, maintenance, and repairs, as well as managing the vehicle's value as it depreciates over time. Understanding how these costs connect is key to making smarter decisions, whether you're considering used cars or comparing features in newer models.

Ownership also comes with legal and practical responsibilities, including registration, maintaining valid auto insurance coverage, and ensuring the vehicle meets Canadian safety and compliance standards. If you're buying from a private seller, reviewing a vehicle history report or CARFAX Canada report can help confirm the vehicle’s condition and ownership history before completing your purchase.

By viewing vehicle ownership as a long-term financial commitment rather than a one-time transaction, you can make more informed decisions that protect both your budget and your investment.

How Much Does Vehicle Ownership Really Cost in Canada?

The true cost of vehicle ownership in Canada goes far beyond your monthly payment. When you factor in insurance, fuel, maintenance, depreciation, and fees, most drivers spend between $8,000 and $15,000 per year, depending on the type of vehicle and driving habits. Data from Statistics Canada consistently shows that transportation is one of the largest household expenses, making it essential to understand the full financial picture before committing to an auto purchase.

The average cost of owning a car in Canada includes monthly payments, insurance, fuel, maintenance, and depreciation. This is often referred to as the total cost of ownership (TCO), which reflects the full financial impact of owning and operating a vehicle over time.

Understanding these costs upfront helps you budget accurately, manage your car ownership expenses, and make smarter financial decisions.

1. Upfront Costs

Before driving off the lot, you’ll need to cover several initial expenses:

- Purchase price or down payment: The largest upfront cost. Whether buying used cars or new cars, a higher down payment reduces long-term interest and monthly payments.

- Taxes and registration fees: Sales tax, licensing, and registration vary by province and can add significantly to your total cost.

- Dealer fees and add-ons: Administrative fees, extended warranty coverage, and protection packages can increase your purchase price if not reviewed carefully during price negotiations.

2. Monthly Loan or Lease Payments

If you finance or lease your vehicle, your monthly payment depends on:

- Vehicle price

- Loan term (typically 3 to 7 years)

- Interest rate based on your credit profile and credit checks

- Loan structure vs car leases

Most payments in Canada range from $400 to $800 per month, though this varies widely based on financing terms and whether you use dealer financing or external lenders.

3. Car Insurance Costs in Canada

Car insurance is mandatory in Canada and varies based on:

- Age and driving experience

- Driving history

- Location

- Vehicle type and safety features

Your policy may include options like collision coverage, which protects your vehicle in the event of an accident but increases your premium. On average, drivers pay $1,500 to $2,500 annually, with higher costs for younger drivers or higher-risk vehicles.

4. Gas Costs in Canada

Fuel is one of the most consistent ongoing costs.

- Fuel-efficient vehicles: $150 to $250 per month

- Larger SUVs or trucks: $300+ per month

- Electric vehicles: lower fuel costs but potential upfront charging expenses

To estimate fuel costs, review the vehicle’s L/100km rating and your expected driving habits.

5. Maintenance Costs for a Car

Routine maintenance is essential for reliability and long-term savings:

- Oil changes, brakes, and tires

- Battery replacements and wear items

- Unexpected mechanical repairs

Vehicles with more advanced vehicle features or luxury components may come with higher repair costs. Most drivers should budget $1,000 to $1,500 annually for maintenance and repairs.

6. Depreciation

Depreciation is one of the largest but least visible costs.

- New vehicles lose 20 to 30 percent of value in the first year

- Up to 50 percent within five years

Researching resale value using tools like Kelley Blue Book or reviewing a CARFAX report can help you make more informed decisions when evaluating long-term value.

7. Registration and Licensing Fees in Canada

Registration and licensing fees vary by province but typically range from $100 to $300 annually. These recurring costs are required to legally operate your vehicle and should always be included in your total ownership budget.

8. Additional Ownership Costs

Other expenses can add up depending on your lifestyle and location:

- Parking fees (especially in urban areas)

- Tolls for commuting routes

- Seasonal expenses like winter tires

- Documentation and renewal fees

These costs are often overlooked but should always be included in your total ownership budget.

What Is the Total Cost of Vehicle Ownership?

Here’s a simplified annual breakdown:

| Expense Category | Estimated Annual Cost |

|---|---|

| Car Payment | $4,800 – $9,600 |

| Insurance | $1,500 – $2,500 |

| Fuel | $1,800 – $3,600 |

| Maintenance & Repairs | $1,000 – $1,500 |

| Registration & Fees | $100 – $300 |

| Depreciation | Varies significantly |

Key Takeaway: Vehicle ownership is a long-term financial commitment, not just a monthly expense. By understanding the full cost picture, including financing, insurance coverage, and depreciation, you can make more informed decisions, reduce financial stress, and avoid unexpected surprises.

What Is Vehicle Depreciation and Why Does It Matter?

Vehicle depreciation refers to how much your car loses value over time, and it’s one of the largest hidden costs of ownership. In Canada, most vehicles lose 20 to 30 percent of their value in the first year and up to 50 percent within five years.

This matters because and how much equity you build in your vehicle. For buyers exploring both new cars and used cars, understanding depreciation can help you choose a vehicle that holds its value better over time.

To reduce the impact, consider buying a used vehicle, choosing models with strong resale value, and planning to keep your car longer to spread out the cost.

How Do You Choose the Right Car for Your Budget and Needs?

Choosing the right car starts with aligning your budget, lifestyle, and long-term ownership goals. The best vehicle isn’t necessarily the newest or most feature-packed, it’s the one you can comfortably afford while meeting your daily needs without creating financial strain.

By following a structured approach, you can narrow your options quickly and make a confident, well-informed decision.

Choosing the right car isn’t just about picking the one that looks the best or has the latest features, it’s about finding a vehicle that fits your lifestyle, financial situation, and long-term ownership goals. Whether buying your first car or upgrading to something new, making an informed decision can save you money and stress down the road.

1. Start With a Realistic Budget

Before exploring vehicles, define what you can truly afford. Your total budget should include:

- Purchase price or down payment

- Monthly loan or lease payments

- Insurance premiums

- Fuel costs

- Maintenance and repairs

As a general guideline, your total vehicle expenses should stay within 15 to 20 percent of your monthly income.

2. Decide Between New and Used

Choosing between new and used vehicles depends on your financial priorities and risk tolerance.

Buying new:

- Full manufacturer warranty

- Latest safety and technology features

- Higher upfront cost and faster depreciation

Buying used:

- Lower purchase price

- Slower depreciation

- Potential for higher maintenance if not inspected properly

For tighter budgets, a certified pre-owned vehicle often offers the best balance between cost and reliability.

3. Match the Vehicle to Your Lifestyle

Your daily driving habits should guide your decision. Ask yourself:

- How often do you drive and how far?

- Do you need cargo space or passenger capacity?

- Will you be driving in winter conditions?

- Is fuel efficiency a priority?

Quick examples:

- City driving: compact cars or hybrids

- Long commutes: fuel-efficient sedans

- Families: SUVs or minivans

- Outdoor use: trucks or AWD vehicles

Choosing based on lifestyle prevents overpaying for features you don’t need.

4. Understand Your Payment Option

How you pay for your vehicle affects both short-term affordability and long-term value.

Financing:

- You own the vehicle once the loan is paid off

- No mileage restrictions

- Higher monthly payments but builds equity

Leasing:

- Lower monthly payments

- Mileage limits and usage restrictions

- No ownership at the end of the term

Financing is generally better for long-term value, while leasing suits those who prefer lower payments and newer vehicles more frequently.

5. Consider Fuel Efficiency and Long-Term Costs

Fuel economy has a direct impact on your ongoing expenses.

- Lower L/100km ratings mean better fuel efficiency

- Hybrids and electric vehicles reduce fuel costs over time

- Larger vehicles typically cost more to operate

A vehicle that seems affordable upfront can become expensive if fuel consumption is high.

6. Prioritize Safety and Reliability

A lower purchase price means little if the vehicle is unreliable or unsafe. Focus on:

- Crash test ratings

- Advanced safety features

- Brand reliability history

Vehicles from manufacturers like Toyota, Honda, and Subaru are consistently recognized for long-term reliability.

7. Research and Test Drive Before You Decide

Before committing:

- Read expert and owner reviews

- Compare resale values

- Get insurance quotes in advance

- Test drive multiple vehicles

Pay attention to comfort, visibility, handling, and overall driving experience.

Key Takeaway:Choosing the right car is about balancing affordability, reliability, and lifestyle fit. Taking the time to evaluate your options carefully can save you thousands and lead to a more confident vehicle ownership experience.

Should You Finance, Lease, or Buy a Car Outright?

The best way to pay for a vehicle depends on your budget, driving habits, and long-term financial goals. In Canada, most drivers choose between financing, leasing, or paying cash, each option impacts your total cost, flexibility, and ownership differently.

Understanding how each option works helps you choose the path that fits your lifestyle while avoiding unnecessary costs.

What’s the Difference Between Financing, Leasing, and Paying Cash?

Financing (car loan):

- You make monthly payments and own the vehicle once the loan is paid off

- No mileage restrictions

- Builds equity over time

Leasing:

- You pay to use the vehicle for a fixed term (typically 2 to 5 years)

- Lower monthly payments

- Mileage limits and return conditions apply

- No ownership unless you buy at the end

Paying cash:

- No monthly payments or interest

- Immediate full ownership

- Requires a larger upfront investment

Financing is generally better for long-term value, while leasing suits those who prefer lower payments and newer vehicles more frequently.

Pros and Cons of Financing, Leasing, and Paying Cash

Pros and Cons of Financing a Vehicle

Pros:

- Full ownership after the loan is paid

- No mileage limits or restrictions

- Better long-term value compared to leasing

Cons:

- Higher monthly payments

- Responsible for depreciation

- Maintenance costs increase after warranty expires

Best for: drivers planning to keep their vehicle long-term or drive higher annual mileage.

Pros and Cons of Leasing a Vehicle

Pros:

- Lower monthly payments

- Access to newer vehicles more often

- Typically lower repair costs during the lease term

Cons:

- No ownership or equity

- Mileage limits and overage fees

- Potential charges for wear and tear

Best for: drivers who prefer lower monthly payments and upgrading vehicles every few years.

When Does Paying Cash Make Sense?

Paying cash is often overlooked but can be a strong financial option if you have the savings available.

Best suited for:

- Buyers who want to avoid interest costs

- Those with stable savings and emergency funds

- Lower-priced or used vehicle purchases

Note: tying up a large amount of cash in a depreciating asset may limit financial flexibility.

Financing vs Leasing, Which Costs Less?

Over time, financing is typically more cost-effective because you eventually stop making payments and retain ownership value.

Leasing may appear cheaper monthly, but continuous leasing cycles can result in higher long-term costs without building equity.

How to Choose the Right Option for You

| Factor | Financing (Loan) | Leasing | Paying Cash |

|---|---|---|---|

| Monthly Budget | Higher monthly payments | Lower monthly payments | No monthly payments |

| Upfront Cost | Down payment typically required | Lower upfront cost | High upfront cost |

| Ownership | You own the vehicle after payoff | No ownership unless you buy at end | Immediate full ownership |

| Long-Term Cost | Lower over time | Higher if leasing repeatedly | Lowest overall (no interest) |

| Mileage Needs | Unlimited driving | Mileage limits apply | Unlimited driving |

| Flexibility | Can sell or trade anytime | Restrictions and end-of-lease terms | Full control |

| Vehicle Preference | Best for long-term ownership | Best for driving new vehicles often | Best for budget-conscious buyers |

| Best For | Long-term savings and ownership | Lower payments and short-term use | Avoiding debt and interest |

Key Takeaway: There’s no one-size-fits-all answer. Financing offers long-term value and ownership, leasing provides flexibility and lower payments, and paying cash eliminates interest entirely. The right choice depends on how you balance affordability, flexibility, and long-term financial goals.

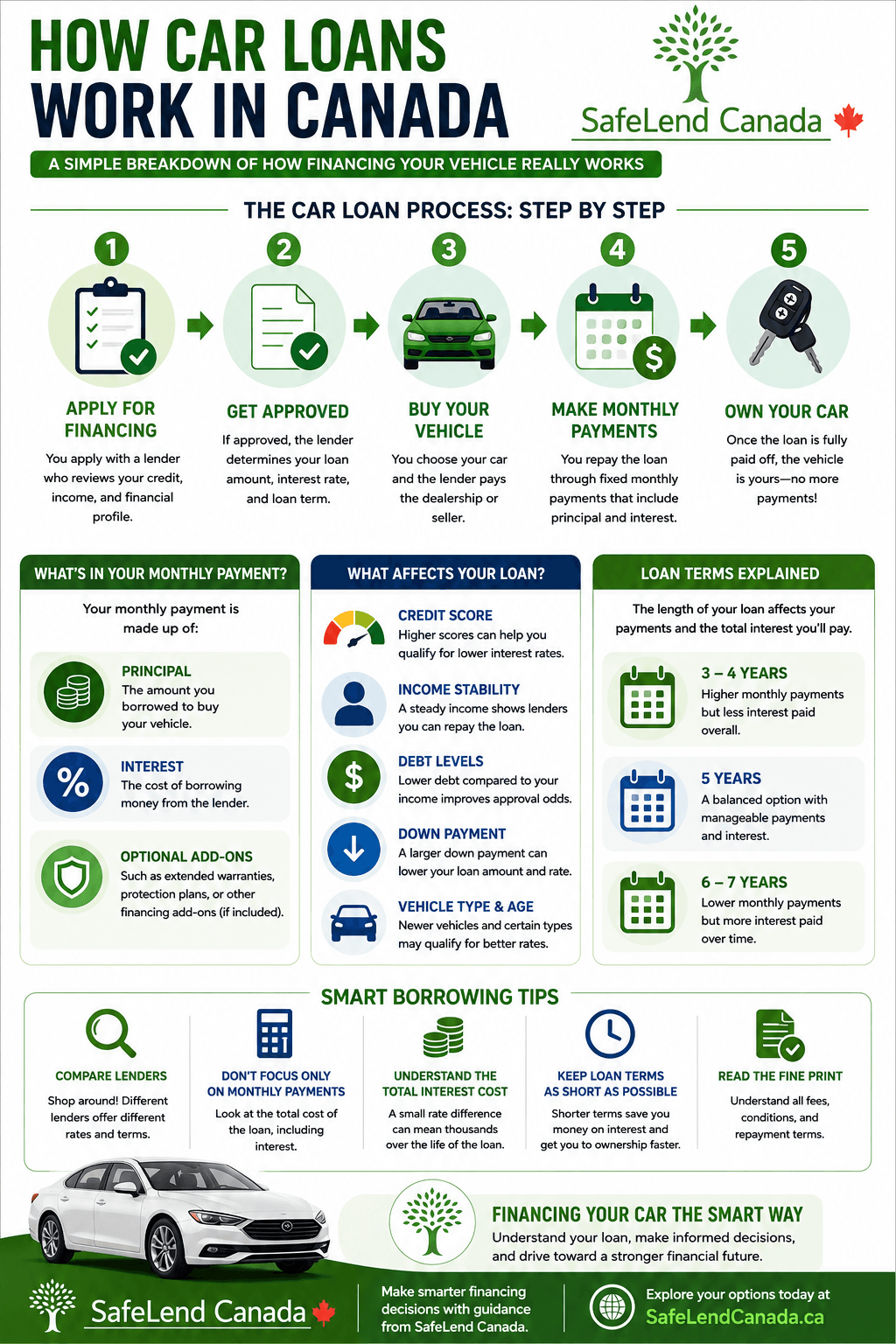

How Do Car Loans Work in Canada?

A car loan allows you to finance a vehicle by borrowing money from a lender and repaying it over time with interest. In Canada, loan terms, interest rates, and approval decisions are based largely on your credit profile, income, and the value of the vehicle you’re purchasing.

Understanding how car loans work helps you secure better terms, avoid overpaying, and make confident financing decisions.

What Is a Car Loan and How Does It Work?

When you take out a car loan:

- A lender pays the dealership or seller on your behalf

- You repay the loan through fixed monthly payments

- Each payment includes both principal and interest

- The loan term typically ranges from 3 to 7 years

Until the loan is fully paid off, the lender may hold a lien on the vehicle.

What Factors Affect Your Car Loan Approval?

Lenders evaluate several key factors before approving your loan:

- Credit score and credit history

- Income and employment stability

- Debt-to-income ratio

- Down payment amount

- Vehicle age and condition

Stronger financial profiles typically qualify for lower interest rates and better loan terms.

How Are Car Loan Interest Rates Determined?

Interest rates in Canada vary depending on both market conditions and your personal financial profile.

- Higher credit scores usually mean lower rates

- Longer loan terms often result in higher total interest paid

- New vehicles may qualify for lower rates than used vehicles

Even a small difference in interest rate can significantly impact your total cost over time.

What Is a Typical Car Loan Term in Canada?

Most car loans fall within these ranges:

- Short-term loans (3–4 years): higher payments, less interest paid

- Mid-term loans (5 years): balanced option for most buyers

- Long-term loans (6–7 years): lower monthly payments, higher total cost

Choosing the right term depends on balancing affordability with long-term savings.

What Is a Car Loan Payment Made Of?

Each monthly payment includes:

- Principal: the amount borrowed

- Interest: the cost of borrowing

- Optional add-ons: warranties or protection products (if included in financing)

Understanding this breakdown helps you see how much you’re actually paying over time.

What Happens If You Miss Payments?

Missing payments can have serious consequences:

- Negative impact on your credit score

- Late fees and additional interest

- Risk of vehicle repossession

Staying consistent with payments is critical to protecting your financial health.

Key Takeaway: Car loans are structured to make vehicle ownership more accessible, but the terms you receive can significantly impact your total cost. By understanding how loans work and what lenders look for, you can position yourself to secure better rates and more manageable payments.

What Mistakes Should First-Time Car Buyers Avoid?

First-time car buyers often focus on getting approved or finding the right vehicle, but the biggest financial mistakes happen in the details. From overlooking total costs to rushing financing decisions, these missteps can cost thousands over time. Understanding what to avoid is just as important as knowing what to do.

Quick Summary: Mistakes to Avoid

- Focusing only on monthly payments

- Choosing long loan terms without understanding total cost

- Not comparing insurance and financing options

- Ignoring depreciation and resale value

- Skipping inspections or test drives

- Paying for unnecessary add-ons

- Not planning for maintenance

1. Focusing Only on the Monthly Payment

Looking only at the monthly payment can hide the true cost of a vehicle.

What goes wrong:

- Longer loan terms reduce payments but increase total interest

- Key expenses like insurance, fuel, and maintenance are overlooked

How to avoid it:

- Keep total vehicle costs within 15 to 20 percent of your monthly income

- Focus on total cost of ownership, not just the payment

- Get pre-approved before shopping

2. Choosing the Wrong Loan Terms

Financing decisions can significantly impact how much you pay over time.

What goes wrong:

- Extending loan terms (6 to 8 years) to lower payments

- Accepting the first offer without comparing lenders

- Misunderstanding promotional rates or hidden costs

How to avoid it:

- Aim for loan terms of 5 years or less when possible

- Compare multiple lenders before committing

- Review the total interest cost over the full term

3. Not Checking Insurance Costs in Advance

Insurance can vary significantly depending on the vehicle.

What goes wrong:

- Choosing vehicles with high premiums

- Not factoring in age, location, or driving history

- Getting quotes after committing to a purchase

How to avoid it:

- Get quotes for multiple vehicles before deciding

- Choose models with strong safety ratings

- Bundle policies where possible to reduce costs

4. Overlooking Depreciation and Resale Value

Depreciation is one of the largest long-term costs of ownership.

What goes wrong:

- Buying new vehicles that lose value quickly

- Choosing models with poor resale value

- Not planning for future trade-in or sale

How to avoid it:

- Consider used or certified pre-owned vehicles

- Research brands with strong resale value like Toyota, Honda, and Subaru

- Plan to keep your vehicle long enough to offset depreciation

5. Skipping the Test Drive and Inspection

A vehicle that looks good on paper may not perform well in real life.

What goes wrong:

- Buying without a proper test drive

- Skipping a professional inspection on used vehicles

- Missing signs of mechanical or safety issues

How to avoid it:

- Test drive multiple vehicles

- Get a pre-purchase inspection for used cars

- Watch for unusual sounds, handling issues, or discomfort

6. Paying for Unnecessary Add-Ons

Dealer add-ons can significantly increase your total cost.

What goes wrong:

- Buying extended warranties or protection packages without research

- Paying for duplicate coverage

- Adding thousands to the final price unnecessarily

How to avoid it:

- Decide in advance what you actually need

- Decline extras you didn’t plan for

- Compare third-party options if considering warranties

7. Underestimating Maintenance Costs

Ongoing maintenance is part of long-term ownership.

What goes wrong:

- Choosing vehicles with high repair costs

- Skipping routine maintenance

- Not budgeting for unexpected repairs

How to avoid it:

- Budget $1,000 to $1,500 annually for maintenance

- Choose reliable vehicles with lower repair costs

- Follow recommended service schedules

Key Takeaway: Avoiding these common mistakes can save you thousands and make your vehicle ownership experience far more predictable. The most successful buyers take a long-term approach, focusing on total cost, financing structure, and reliability rather than just the initial purchase.

What Are the Hidden Costs of Vehicle Ownership (And How Can You Prepare)?

The cost of owning a car goes beyond the purchase price and monthly payment. Many expenses aren’t immediately obvious, but they can add up quickly and impact your long-term budget. Understanding these hidden costs helps you plan ahead and avoid financial surprises.

Quick Overview: Hidden Costs to Watch For

- Depreciation

- Insurance increases

- Fuel fluctuations

- Maintenance and repairs

- Tires and seasonal expenses

- Parking and tolls

- Licensing and registration fees

1. Depreciation

Why it matters:

Your vehicle loses value over time, often faster than expected.

- 20 to 30 percent loss in the first year

- 20 to 30 percent loss in the first year

How to prepare:

Consider used or certified pre-owned vehicles

- Choose brands with strong resale value like Toyota, Honda, and Subaru

- Plan to keep your vehicle longer to offset value loss

2. Insurance Premium Changes

Why it matters:

Insurance costs can vary widely and increase over time due to

- higher rates for certain vehicles/locations

- Premium increases after tickets or claims

How to prepare:

- Get quotes before buying

- Compare multiple providers

- Look for bundling or safe driving discounts

3. Fuel Cost Fluctuations

Why it matters:

- Fuel is a variable cost that can rise unexpectedly.

- Smaller cars: typically $150 to $250 per month

- Larger vehicles: $300 or more per month

How to prepare:

- Check fuel efficiency ratings (L/100km)

- Consider hybrid or electric options

- Adjust driving habits to improve efficiency

4. Maintenance and Unexpected Repairs

Why it matters:

- Routine maintenance and repairs are unavoidable over time.

- Oil changes, brakes, tires, and batteries

- Higher costs as the vehicle ages

How to prepare:

- Budget $1,000 to $1,500 annually

- Follow maintenance schedules

- Plan ahead for out-of-warranty repairs

5. Tires and Seasonal Costs

Why it matters:

- Tires are a recurring and often underestimated expense.

- Winter tires required in some provinces

- Replacement every 3 to 5 years

How to prepare:

- Budget for seasonal tire changes

- Rotate tires regularly to extend lifespan

- Factor in storage if needed

6. Parking and Tolls

- Urban driving often includes additional recurring costs.

- Parking: $100 to $300 per month in some cities

- Tolls can add up for daily commuters

How to prepare:

- Research local parking costs

- Consider commuting alternatives

- Look for permits or discounted options

7. Licensing and Registration Fees

Why it matters:

- These are recurring costs required to legally operate your vehicle.

- Annual registration fees vary by province

- Late renewals can lead to penalties

How to prepare:

- Budget for yearly renewals

- Set reminders to avoid fines

- Check provincial requirements in advance

Key Takeaway: Hidden costs can significantly impact the true cost of vehicle ownership. By planning for these expenses early, you can make more informed decisions, stay within budget, and avoid unexpected financial pressure.

What Are the Steps to Buying a Car in Canada?

For any first time car buyer Canada, following a structured process can help avoid costly mistakes and improve your overall experience.

- Set your budget and get pre-approved

- Research vehicles and compare options

- Check pricing using tools like Kelley Blue Book

- Review vehicle history (CARFAX Canada)

- Test drive and inspect

- Negotiate price and financing

- Finalize paperwork and registration

Final Thoughts: How Can You Make a Smart Car Buying Decision?

Making a smart car buying decision comes down to understanding the full picture and the total cost of owning a car, not just the purchase price or monthly payment. Vehicle ownership includes ongoing responsibilities like insurance, maintenance, financing, and long-term value, all of which impact your overall financial health.

Before moving forward, take a step back and ask yourself:

- Can I comfortably afford both upfront and ongoing costs?

- Do I understand how different financing options, including loans or a finance lease, will impact me long-term?

- Have I considered insurance, maintenance, and depreciation?

- Am I choosing a vehicle that fits my lifestyle, not just my preferences?

Taking the time to answer these questions helps you avoid common mistakes and make more confident decisions.

Whether you’re buying through a dealership or a private sale, preparation is key. Comparing options, reviewing your credit score, and understanding when a co-signer loan may be required can help improve your approval chances and overall financing experience.

Staying informed about requirements set by organizations like Transport Canada and keeping your documentation organized will also ensure a smoother ownership process from start to finish.

By focusing on total cost, long-term value, and your personal needs, you can make informed decisions that lead to a more predictable and stress-free vehicle ownership experience.

Frequently Asked Questions About Vehicle Ownership Costs

What are the biggest hidden costs of vehicle ownership?

The most common hidden costs include depreciation, insurance, fuel, maintenance, repairs, parking, and registration fees. These expenses often go unnoticed at first but can significantly increase the total cost of ownership over time.

How much should I budget for car maintenance each year?

Most drivers should budget $1,000 to $1,500 per year for routine maintenance and unexpected repairs. This includes oil changes, brakes, tires, and minor mechanical issues.

Why is car insurance more expensive for first-time buyers?

Insurance is typically higher for new drivers due to limited driving history and higher perceived risk. Costs also vary based on your location, vehicle type, and driving record.

How can I reduce fuel costs?

To lower fuel expenses: choose a vehicle with strong fuel efficiency (low L/100km), drive smoothly and avoid aggressive acceleration, keep tires properly inflated, and consider hybrid or electric vehicles for long-term savings.

Is it better to buy a new or used car for long-term savings?

Used vehicles are often more cost-effective because they avoid the steep depreciation of new cars. However, new vehicles may offer warranties and lower short-term maintenance costs. The best choice depends on your budget and how long you plan to keep the vehicle.

How do I prepare for unexpected car expenses?

Set aside an emergency fund for repairs and maintenance. A good guideline is saving $100 per month to cover unexpected costs like tire replacements, battery issues, or repairs.

How much does depreciation really affect a car’s value?

Depreciation is one of the largest ownership costs. Most vehicles lose up to 50 percent of their value within five years, with the biggest drop occurring in the first year.

Do electric vehicles (EVs) have lower ownership costs?

Electric vehicles typically have lower maintenance costs since they require fewer mechanical repairs. However, they may have higher upfront costs and require charging setup, so total savings depend on usage and local energy rates.

What are some common mistakes first-time car buyers make?

Common mistakes include: focusing only on monthly payments, not comparing insurance costs, choosing inefficient or expensive vehicles to maintain, skipping inspections or maintenance, and paying for unnecessary add-ons.

How do I calculate the total cost of owning a car in Canada?

To estimate total cost, include: insurance, fuel, maintenance and repairs, registration and fees, and depreciation. Using a car cost calculator can help you estimate these expenses before buying.

What’s the best way to avoid overspending on a car?

To stay within budget: choose a vehicle that fits your financial situation, keep loan terms as short as possible, budget for all ownership costs, maintain your vehicle regularly, and set aside an emergency fund.

By planning ahead and making informed choices, you can enjoy the benefits of vehicle ownership without the financial headaches! 🚗💡

Important Note: This article and its resources are purely for informational use. They do not reflect the offerings of specific companies or lenders. Our goal is to provide knowledge and insights for better financial decision-making. We recommend conducting in-depth research and seeking professional advice before making any financial decisions. SafeLend Canada, while not a lender, collaborates with various lenders to assist clients in refinancing their auto loans.